Ideal Assets for Tokenization – P.4: What Makes an Asset Tokenization-Friendly?

Let’s dive in with a friendly, global perspective to understand what traits make an asset tokenization-ready.

In our journey through tokenization, we've explored how regulatory environments (Part 1), market frictions (Part 2.1 & 2.2), and investor demand (Part 3) shape the landscape. Now, in Part 4, we focus on the intrinsic characteristics that make certain assets prime candidates for tokenization—and why some assets thrive on-chain while others remain challenging.

Key Characteristics of Tokenization-Friendly Assets

Tokenization isn't a one-size-fits-all process. Certain traits significantly influence an asset’s tokenization potential:

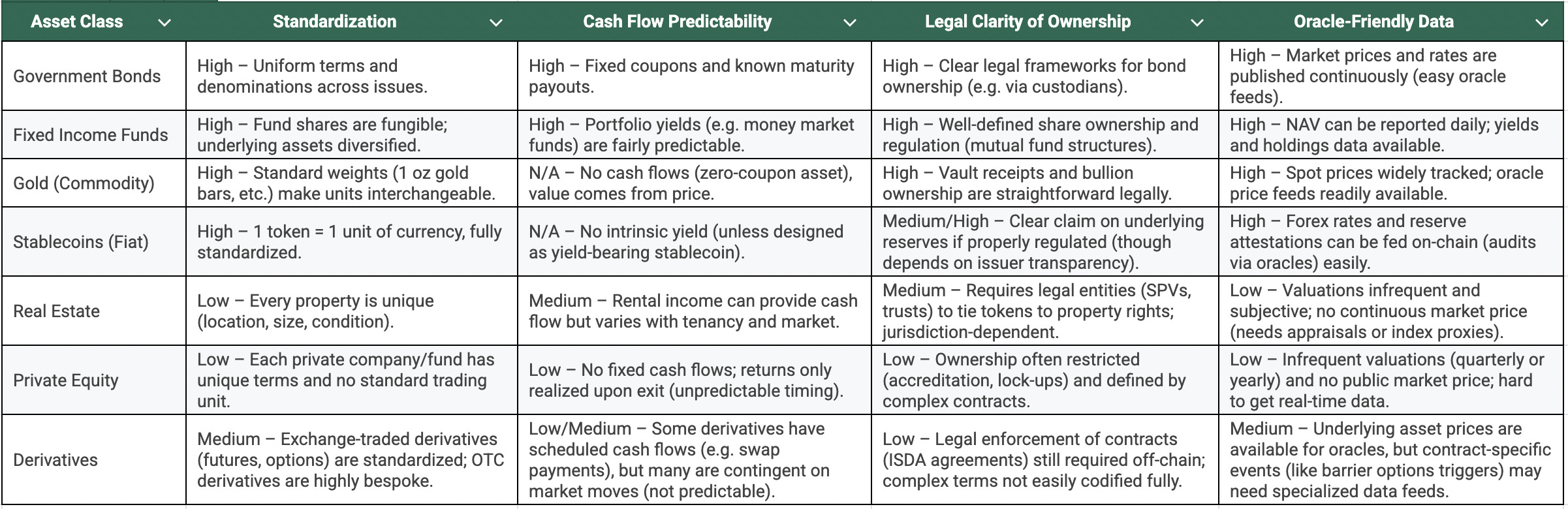

Standardization: Assets that are uniform and fungible are easiest to tokenize. Government bonds and gold are prime examples, as bonds have standard denominations and terms, and gold trades in consistent weights (like ounces). This uniformity simplifies creating interchangeable tokens. Conversely, real estate lacks standardization since each property is unique, complicating its tokenization.

Predictable Cash Flows: Assets with steady, known income streams attract early tokenization due to simplicity and smart contract compatibility. Fixed-income securities, such as bonds, exemplify this—they offer regular, predictable interest payments and a clear principal repayment at maturity. Predictable cash flows make it straightforward to program automatic distributions and simplify valuation. By contrast, startup equity has uncertain returns, creating challenges for direct tokenization because it lacks regular, predictable payouts, relying instead on future uncertain events like an exit or IPO.

Legal Clarity of Ownership: Clearly defined and enforceable ownership significantly reduces tokenization friction. Tokens essentially represent ownership claims, best suited to assets with robust legal recognition. Gold tokens, for example, often represent direct legal claims on physically stored gold, providing clear ownership. Similarly, tokenized bond funds typically have straightforward legal structures for investors' claims. Real estate, however, involves jurisdiction-specific laws and complex registries, necessitating additional legal wrappers like LLCs or trusts to clarify ownership rights. As the IMF highlights, tokenizing complex assets like derivatives doesn't remove existing legal intricacies or enforcement challenges, limiting their early on-chain adoption.

Oracle Compatibility (Reliable Data Availability): Blockchain tokens require accurate external data ("oracle data") for valuation and operational automation. Assets with transparent, regularly updated market prices (such as bonds and commodities like gold) easily integrate with blockchain through trusted oracle services (e.g., Chainlink). Conversely, assets with infrequent or subjective valuations—like private businesses, real estate, or art—face significant challenges. The absence of continuous, trustworthy price data means more manual intervention is needed, diminishing blockchain's automation benefits.

In short, tokenization works best with standardized assets offering predictable cash flows, clear legal ownership, and easily accessible, reliable data. Bonds, gold, and certain funds meet these criteria, explaining their early success in tokenization. Conversely, real estate, private equity, and derivatives face greater complexity, requiring innovative approaches to overcome their inherent tokenization hurdles.

~~~

Let's see how different asset classes measure up against these traits:

As we can see, assets with simple, well-defined structures (bonds, funds, commodities) check most of the boxes. They are fungible, produce either steady income or have transparent pricing, come with clear legal ownership, and can be easily interfaced with through oracles. This explains why these assets were among the first to be successfully tokenized on a meaningful scale. Meanwhile, assets that are unique, illiquid, or legally convoluted (real estate, private investments, bespoke derivatives) tend to score low on multiple dimensions, meaning extra friction to tokenize.

Why Bonds, Funds, and Gold Led the Charge

The early tokenization successes—government bonds, fixed-income funds, and gold—clearly check the boxes of standardization, predictable returns, clarity of ownership, and robust oracle data.

Government Bonds offer ideal tokenization traits: they're standardized, highly liquid, and carry predictable cash flows. Institutions quickly embraced tokenized U.S. Treasuries and money market funds (MMFs), exemplified by products like BlackRock’s BUIDL and Franklin Templeton’s OnChain Fund. These instruments provided investors with stable, transparent yields coupled with blockchain's instant settlement and continuous liquidity.

Other Fixed-Income Funds have also found success in tokenization. For instance, WisdomTree has introduced a suite of 13 tokenized fixed-income funds, including the WisdomTree Long Term Treasury Digital Fund (TWLGX), WisdomTree Floating Rate Treasury Digital Fund (FLTTX) and the WisdomTree Short-Duration Income Digital Fund (WTSIX). These funds offer investors exposure to various fixed-income strategies, providing stable returns while leveraging blockchain's benefits of enhanced liquidity and accessibility.

Gold, long regarded as a safe-haven asset, proved particularly well-suited to tokenization. Physical gold already trades in standardized units, making it straightforward to represent digitally. Tokens like Paxos Gold (PAXG) and Tether Gold (XAUT) allow investors easy, fractional ownership of gold, providing instant liquidity, transparent pricing, and clear legal custody structures. The global trust and recognized valuation mechanisms for gold accelerated investor acceptance.

These assets thrived because their real-world complexities were minimal, making blockchain integration efficient and investor-friendly. These assets initially thrived because blockchain effectively streamlined existing, simple structures rather than complicating them. Early tokenization success depended heavily on assets having minimal legal, operational, and valuation complexities. Bonds, funds, and gold perfectly matched this profile, setting clear benchmarks for other assets.

Complex Assets, Higher Friction: Real Estate, Private Equity, and Derivatives

While bonds, gold, and fixed-income funds rapidly embraced tokenization, assets like real estate, private equity, and derivatives have lagged due to inherent complexities.

Real Estate is notoriously challenging for tokenization. Each property is unique in location, size, quality, and valuation, making standardization difficult. Legal ownership also adds complexity; real estate laws and title registries differ significantly across jurisdictions, complicating blockchain-based transfers. Tokenizing real estate typically requires intermediary structures (e.g., LLCs or trusts), which introduce off-chain legal complexities and reduce blockchain's efficiency benefits. Platforms such as RealT have succeeded with fractional ownership of rental properties, but widespread adoption remains elusive due to these challenges.

Private Equity (PE) faces similar hurdles. Investments in PE typically involve bespoke terms, complex shareholder agreements, and uncertain cash flows, making standardization nearly impossible. Valuation transparency is another major issue; PE assets are often appraised infrequently and subjectively, limiting their oracle compatibility. Although platforms like Securitize and Tokeny have started tokenizing PE funds—allowing fractional ownership and lower investment thresholds—the intricacies of investor rights, illiquid secondary markets, and regulatory restrictions continue to limit broader acceptance.

Derivatives present perhaps the highest complexity of all. These financial instruments rely heavily on contingent outcomes (e.g., options or swaps), making cash flows uncertain and difficult to automate via smart contracts. Their legal and operational structures often require off-chain enforcement, specialized counterparties, and frequent manual intervention, negating blockchain’s automation advantages. While protocols like Synthetix and Lyra are pioneering on-chain derivatives, they typically rely on crypto-native underlying assets. Traditional derivatives involving equities, bonds, or commodities still grapple with off-chain dependencies and significant regulatory scrutiny, slowing tokenization progress.

Additionally, all three asset classes suffer from limited oracle compatibility. Reliable, continuous, and transparent valuation data is scarce, requiring substantial manual intervention and off-chain oversight. Unlike publicly traded bonds or commodities, these assets lack readily accessible market data feeds, significantly complicating their integration with blockchain oracles.

Yet despite these challenges, demand for tokenization persists. Investors and institutions continue exploring innovative solutions—like regulatory sandboxes and hybrid structures—to navigate these complexities. Ultimately, real estate, private equity, and derivatives may require fundamental industry shifts or significantly simplified product designs to fully realize blockchain’s potential.

Indirect Exposure: The Stablecoin Gateway

Interestingly, while direct tokenization of complex assets remains challenging, investors have widely embraced stablecoins as indirect gateways to real-world asset exposure. Stablecoins indirectly link holders to traditional assets like government bonds through reserve backing, allowing users simplified yet secure exposure to stable, yield-generating assets. According to RWA.xyz (6 May, 2025)

Stablecoins USDT and USDC now dominate tokenized assets, representing over 90% of the market.

Directly tokenized RWAs (private credit, treasuries, real estate, ect) currently comprise about 7.76%, amounting to approximately $19.4 billion.

A classic example is the stablecoin you likely already know: many fiat-backed stablecoins like USDC or USDT hold a significant portion of their reserves in government bonds (e.g., US T-bills). Holders of USDC don’t directly own those T-bills, but the reason USDC is stable and trusted is because it’s fully collateralized by cash and high-quality bonds.

Traditionally, the stablecoin model didn’t pass through the bond yield to the end user – the issuing company (like Tether or Circle) kept the interest income to fund operations (and profit). However, there’s a new wave of yield-bearing stablecoins emerging where that yield is passed on to holders. Some noticeable yield-bearing stablecoins we should know:

Ethena’s eUSD, offering direct yield distribution from underlying RWAs. Within four months of launch, eUSD achieved a market cap of $2.3 billion – showing the massive appetite for a dollar token that also yields a return.

Mountain Protocol’s USDM or Overnight Finance’s yield USD – these aim to maintain a $1 peg while investing reserves into low-risk RWA to generate interest, which is then paid to token holders.

PayPal’s new PYUSD stablecoin, while not currently paying out interest, is positioned to use safe assets (cash, bonds)

And we have come to the end of the series.

This series illuminated how tokenization is reshaping financial markets by leveraging regulatory clarity, reducing market frictions, and responding to investor demands. Yet, asset characteristics ultimately define tokenization success.

Assets like government bonds and gold thrived early due to intrinsic simplicity and clarity. Complex assets like real estate and derivatives continue to evolve, driven by investor demand and innovation, despite their inherent challenges.

Stablecoins emerged as indirect but powerful bridges, illustrating how tokenization adapts creatively to market needs. They exemplify tokenization's potential—not just as a digital wrapper for assets, but as a fundamental evolution in financial accessibility and efficiency.

Tokenization is poised to gradually transform finance on a global scale, one asset at a time, as the lessons learned from early projects inform the next wave. We as investors and enthusiasts are witnessing the bridging of worlds: TradFi meeting DeFi, dollars meeting crypto, and illiquid assets becoming liquid. The genie is out of the bottle, and as tech and regulation catch up to each other, the list of ideal assets for tokenization will only grow.

Disclaimer: This content is for informational and research purposes only. DYOR!